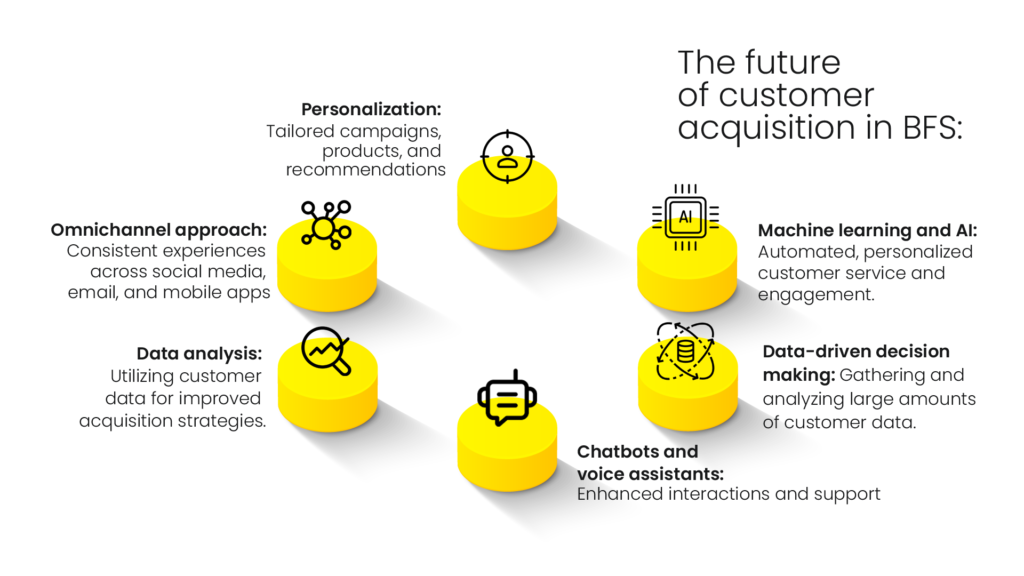

Data, as always, is proving to be the real game-changer for BFS (banking and financial sector) companies. Analytics is driving higher efficiencies and benefits for BFS players, including debt collection. What is the role of analytics in BFSI debt collection? Here’s finding out. With regard to better engagement with consumers for debt collection, BFS players have always depended on conventional models including phone calls and emails/letters. The aim here is application in bulk, which has often led to several experiences that are not as pleasant for both parties (borrowers and lenders). Customers now expect increasing personalisation with diverse requirements and preferences. By tapping machine learning, AI, and predictive analytics, companies are now acting on data-based insights while resolving several problems across sectors, including debt collections. It has led to simpler, faster, and easier systems and procedures for consumers and banks alike, with advanced data science abilities providing teams cutting-edge tools that they require for higher transparency and standardising operational processes. How is data analytics transforming debt collections for BFS entities? Here are some of the ways in which analytics is gradually revolutionising debt collections for banks and financial service providers. A. Building custom outreach strategies- Debt collection is not only about physically reaching out to borrowers. The blueprint has to be wider today, in sync with fast-changing banking ecosystems. Personalising the outreach to borrowers across types and personas, with stage-based plans across channels (deriving from anticipated consumer responses at each stage) is highly necessary for BFS entities today. Data and analytics is now spurring decision-making throughout the entire value chain of collections, along with saving time, energy, and costs for companies simultaneously. B. Debt resolution strategies- Analytics has enabled better debt resolution blueprints on the basis of insights. These include the following aspects: Risk Classification of Borrowers- ML-based algorithms can accurately forecast the chances of delinquency of borrowers, deploying innumerable parameters as inputs. Due to resource limitations, calling every defaulter is next to impossible, not to mention the need to engage debtors, to avoid future non-payment risks and delinquencies. Hence, analytics is what enables hyper-personalisation in this case, enabling agents to communicate the right message in specific scenarios to particular groups of customers. Channel Forecasts- On the basis of insights on earlier communication and behaviour of customers, BFS companies can predict the suitable template, channel, frequency, language, and time to contact borrowers. Several borrowers also prefer digital communication and their preferences may be better identified by algorithms. Optimising Blueprints- Tracking real-time borrower behaviour throughout multiple channels enables the creation of a personalised blueprint and mechanism for debt collection. Predicting Intent-to-Pay– It encompasses forecasting the willingness of borrowers to repay the money, based on outreach measures and historical measures for working out the priorities for the coming day in terms of tele-calling or other outreach initiatives. Internal transaction information, when fused with other factors and behavioural triggers can predict delinquencies, while enabling BFS companies to accurately build pro-active strategies for customer outreach. For instance, lenders may swiftly gain a perspective of customers’ aggrieved/negative reactions or reducing account balance and their inter-relationships. Better Borrower Understanding- Using analytics for debt collections will enable an examination of transactional, demographic, and behavioural information. This will help BFS players gain a better understanding of consumers, while identifying specific patterns and getting insights that help them develop strategic blueprints for collections. Monitoring borrower responses to several types of messages is also helpful in determining ideal frequencies for interaction and suitable timelines. Risk-driven segmentation may also be useful for better targeting. Insight-Driven Debt Collection Decisions- Debt collection decisions can be taken in a better way, driven by analytics-based insights. Segmentation, predictive systems, deep behavioural analysis, and other blueprints are all possible for BFS companies. Insights are helpful for warning banking entities early regarding delinquencies and defaults in the future. It will help banks work out when people are likely to default and come up with custom strategies for mitigating these situations. These insights also help build suitable responses for interactions with borrowers. Issues with continual follow-up communication will be resolved with data-based intelligence. Banking entities will have suitable knowledge for catering to customers with suitable details at the right times. Building Personalised Relationships- Customer relationships and experiences are crucial aspects for all BFS entities. Data-driven insights and analytics may help greatly in both these departments. Lenders can have language/region-based responses for customers. As can be seen, data analytics can completely transform debt collections for banks and financial services players. Data errors, incorrect entry, issues with detecting frauds have been identified and resolved with smart and new-age AI-based tools. At the same time, debt collection can be enhanced greatly through better insights and real-time visibility into the process. From reaching out to customers at the right time and with personalised offerings, to improving engagement and scaling up predictive/forecasting abilities, it enables BFS players to resolve long-standing problems and convert debt collection into a seamless and standardised process. FAQs 1. What is debt collection in BFS? Debt collection refers to the mechanism for collecting and recovering unpaid/due debt from borrowers. 2. What kind of data is collected and analysed for debt collection? The types of data collected and analysed for debt collection include historical customer data on engagement and interactions, behavioural data, preferences, demographic data, socio-economic and macro-economic data, past financial transaction history of customers, and more. 3. What are the benefits of using data analytics in debt collection? There are several benefits of using data analytics for debt collection, including customising communication and outreach with borrowers, predicting/forecasting future chances of defaults and non-payment, working out better debt collection strategies, and standardising the process. 4. Can data analytics help in predicting future defaulters? Data analytics can be immensely helpful in the prediction of future customer defaults, through generating insights on past purchasing behaviour, financial history, transaction history, and many other parameters. This helps banking and financial services companies forecast the likelihood of defaults and take pro-active steps accordingly.