Close shave – Thank your asteroids.

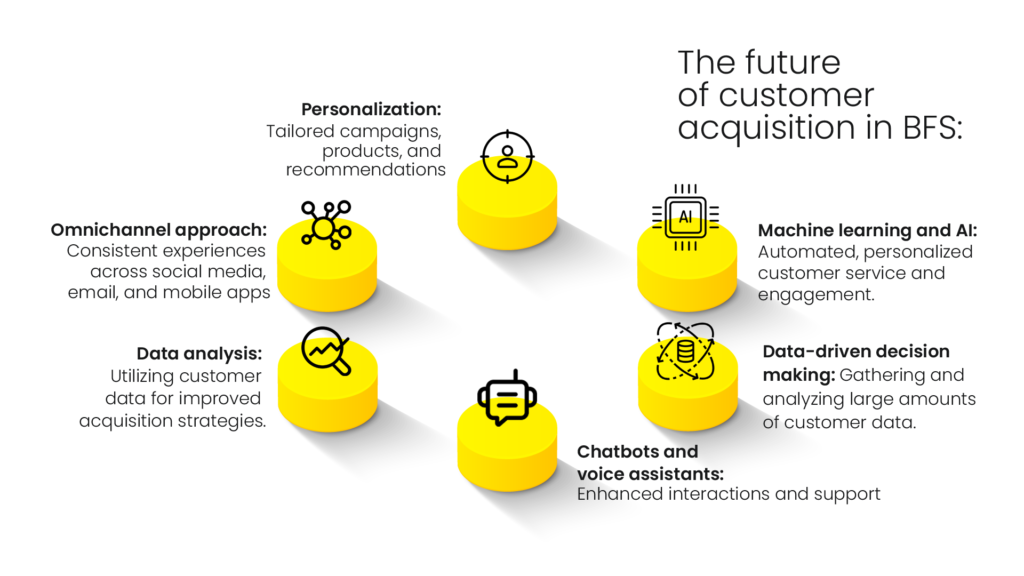

Dear Colleague, we woke up today with a bit of a ‘dinosaur feeling’. 🦖 How Come? The Jurassic emotion was a direct result of finding out that a house-sized asteroid is making a very close pass of our planet today. Fyi, when faced with the wrath of such a rogue rock, the dinosaurs were not so lucky, and that’s evident because these days you are filling up their remains in your car’s fuel tank. 🦖 + ☄️ = ⛽ What’s On The Rocks? As you read this, Asteroid 2018 BG5, a space rock from the Apollo group of near-Earth asteroids, will fly by earth (July 27,2023) at a speed of 30,094 kays an hour, per NASA’s Center for Near-Earth Object Studies (CNEOS). The asteroid will come as close as 4.1 million kilometers to us – a distance which may seem large, but it is relatively small in astronomical terms, considering the vastness of space and the size of the asteroid. Should You Withdraw All Your Savings? No. No. NASA’s best have assured that there is no risk of impact with Earth today or in the foreseeable future. ⚠️ However, even a small asteroid can cause significant damage if it enters the Earth’s atmosphere, as shown by the Chelyabinsk meteor event in 2013, when a 59 feet asteroid exploded over Russia, injuring over 1000 people and damaging nearly 8000 buildings. STATS: Sorry, The Doctor Isn’t Available Life sciences leaders, heads up. Are your sales reps getting the cold shoulder/elbow nudge from doctors more often these days? Turns out, they are not trying to hoodwink your system while catching up on Oppenheimer during office hours. Yeah? How Is That? A new CMI Media Group survey of physicians across countries is providing fresh evidence that face to face meetings with doctors is becoming a rare commodity since COVID-19. When asked, 25% of the doctors reported reducing face-to-face interactions. With another 10% of doctors permanently closing their doors for reps, the survey suggests pharmaceutical companies will find it increasingly tough to put their drugs in front of ~35% of physicians via the traditional in-person route. Aha. What Could Work Then? To start, how doctors utilise their time roughly maps onto the value they place on each touchpoint. Print and online journals are on top, with 79% finding them very or extremely useful. Pharma reps on the other hand, are pretty much down on the attention radar. Only 33% doctors find reps very or extremely useful, placing them below resources like medical websites and unbranded disease education from biopharma. Bonus Data Points 🍎 99% doctors engage with print/online journals or medical websites at least once a month. 🍎 75% also engage with search engines and email, online drug references, direct mailers, medical apps, professional online communities, brand emails, medical videos on YouTube, and medical podcasts. The doctors’ world is clearly leaning towards an omnichannel approach. If you need to explore such a strategy, chat up with Anindya, our resident Life Sciences man. Psst, he curates the most amazing conversations over ☕️. Ai & ANALYTICS: The Chatbot Will See You Now Unlike physicians who are reducing their face time with med reps, did you know chatbots have no pressing personal issues (yet) and are doing mankind some sterling service? I Do This blurb refers to securing consent from humans for stuff like clinical trials and other life sciences related studies, where, hold our battery pack, chatbots are doing very well. Seriously? Yo! Results from a study of the use of a chatbot in the consent process show that it encourages inclusivity, and leads to faster completion of the process with high levels of understanding. On the flip side, the traditional method of securing consent lacks a mechanism to verify understanding objectively, just like all the web forms we give consent to without understanding zilch of the fine print. Comparatively, the chat-based method can test comprehension, disqualifying users who do not show understanding to give consent; rather, it puts them in touch with a genetic counsellor to figure out why knowledge transmission did not occur. Pretty dang smart for a piece of software, talking of which, we have a whole bunch of AI-powered chat bots held in a big steel vault behind Dipak’s office desk. Get in touch with him to deploy one for your business. BFSI: A Single Source of Truth We’ve been swamped with news, stories, videos, and you-name-it, all revolving around artificial intelligence, once prompting OpenAI’s CEO to say, people are ‘begging to be disappointed’ about GPT4, meaning let’s water down the hype, please. But amid all the speculation and noise, what are the most achievable, real world uses of AI? The BFSI Space Is A Great Start, We Say The BFSI sector is flourishing with AI tech integrating with many functions, from the digital KYC verification process to evaluating credit scores. However, to quench the thirst of the customer base accustomed to the convenience of digital tools, the industry needs to deploy more AI tech, the first among them could be; Customised Experience: Because of the very nature of the trade, BFSI players have always had a finger on consumer pulse. Time to take that to the er, bank. Their spending patterns and investment portfolios can assist BFSI businesses to build relevant, personalised messages, enabling them to better present their products and services across various platforms, improving acquisition and loyalty. This is where AI and data analytics shine, delivering value by creating a single source of truth from an ocean of data from within and outside the business. Fraud Detection: While the original BFSI fraud detection model is focused on detecting fraudulent transactions – an area where generative AI has added a powerful weapon to the fraud detection arms depot – a gap remains. You guessed right, detecting fraudulent human behaviour. Fraud does not happen in vacuum or underwater. People commit fraud. AI can also be deployed to comb through the field of behavioural indicators. It’s time to task AI with sifting through the subtleties of human communications — written